Financial & Legal Steps to Setting Up a New Small Business

Starting a small business is exciting.

But figuring out just how many insurance policies you need to protect yourself, wading through tax tricks to save the most money possible…

Not only boring, but hair-raising.

However, it’s this legal and especially financial setup that will have a major impact on your long-term success.

Only about 50% of businesses survive past five years.

One of the biggest reasons for this attrition?

Cash flow stops flowing.

From choosing the right business structure to learning how to effectively separate personal and business finances, there are lots of early decisions you can make to avoid legal snares and cash-leaking mistakes.

This guide will teach you how to protect your personal assets, build credit for your small biz, stay tax-ready, and create a legal and financial foundation that supports scale.

Choosing the Right Business Structure

You’re about to make a really important decision which may be near impossible to change later: how you want to legally structure your business.

We’ll do our best to lay out the basics for you here, but we strongly recommend talking with a business attorney or accountant if you have any doubts or questions at all about getting started. These professionals can help you ensure your choice fits your longer-term business goals.

Why This Is a Crucial First Step

Setting your business up as a partnership, limited liability company (LLC), or corporation all offers varying levels of protections from liability.

Depending on what you decide, if your business faces illegal or financial trouble, your savings, property, and other personal assets may or may not be at risk.

But this isn’t the only thing to consider. Some structures that limit liability don’t have the same tax advantages, have strict requirements, or are complex to set up and maintain.

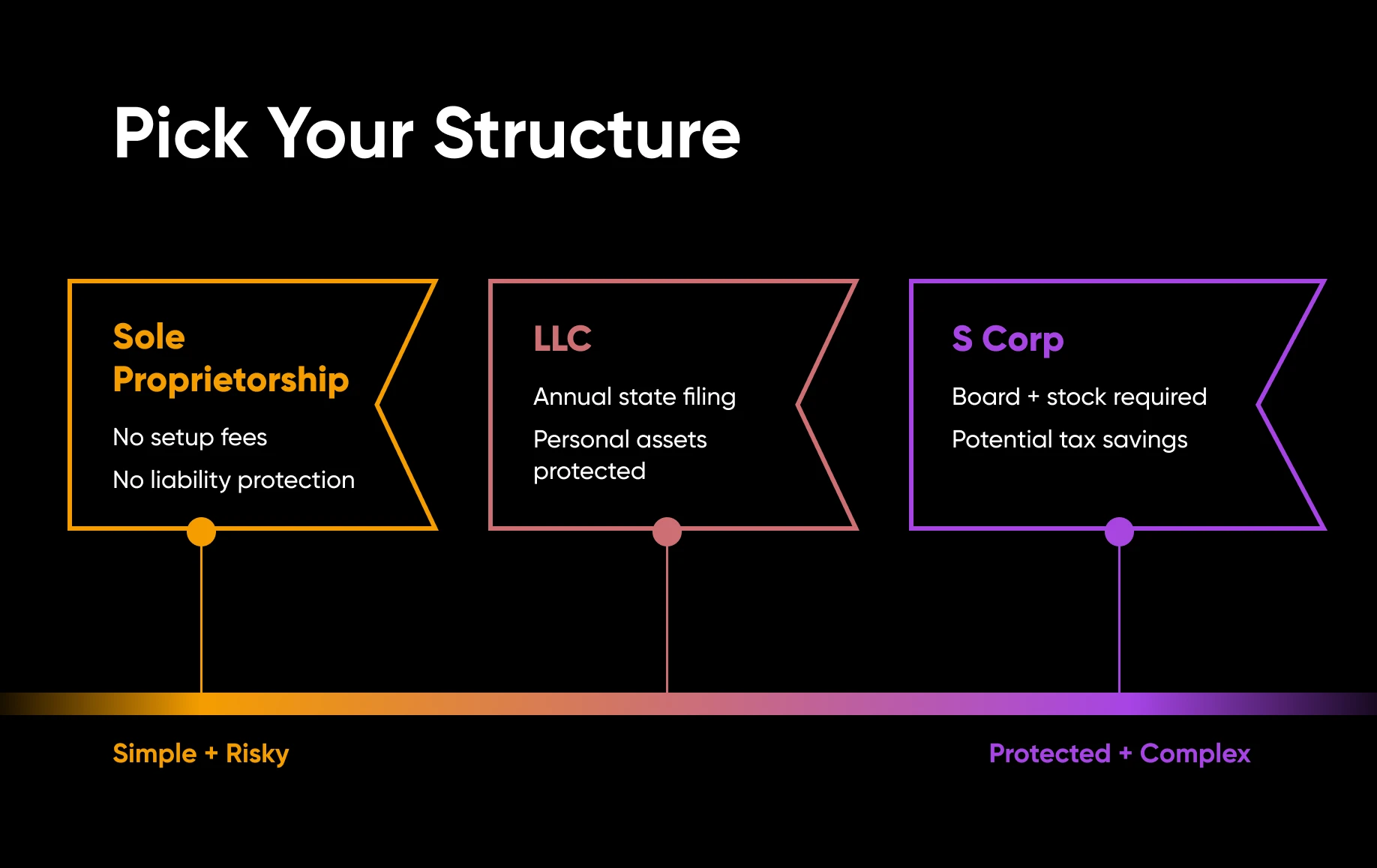

Understand Your Options

Many beginners default to a sole proprietorship.

Why? It’s simple and cheap to start.

But it comes with a major risk: your personal assets aren’t protected.

That means if your business faces a lawsuit or gets into debt it can’t get out of, your savings, car, or even home could be at risk.

A limited liability company is another go-to choice for freelancers and small businesses, especially. While it’s mostly easy to set up and manage, you often have to file papers and pay a fee to the state annually. The main goal people achieve with this option is separating personal and business liabilities.

An S corp is like an LLC, but any owners can be named employees, potentially leading to more favorable self-employment taxes. There are also more rules to follow, such as setting up a board, issuing stock, and more.

All of these structures are pass-through entities, so tax is reported and paid by the owner(s) on their personal tax returns.

These are the most common setups for smaller businesses, but there are tons of other options, workarounds, and details to dig into.

To learn more, the U.S. Small Business Administration (SBA) offers this foundational guide to help you nail this early but critical decision about your business structure.

Match Your Structure to Your Needs

When making this important decision, ask yourself: How much risk can I handle? How much complexity am I willing to manage? What fees can I actually afford right now?

Your answer will help narrow your options.

For example, an individual freelancer might pick an LLC for simple liability protection. A business making six figures with multiple owners and plans to hire a workforce might choose an S corp even with all its regulations in order to save on taxes.

Again, we recommend consulting a professional if you have any questions.

Separating Personal and Business Finances

Mixing personal and business finances is a common mistake first-time business owners make.

Let’s cover why and how to avoid this misstep.

Why Financial Clarity Is Key

Keeping finances separate protects you and your business in a couple of key ways.

Stay out of Legal Trouble

Simply put, clear financial records make tax filing easier, thus reducing the risk of errors that could trigger an audit.

If your accounts are mixed, it becomes difficult to prove which expenses are business-related. This could lead to denied deductions, penalties, or even legal disputes.

Separate accounts also protect your personal assets, which is the whole point of an LLC.

In the event of a lawsuit or debt collection, having distinct accounts makes it easier to demonstrate that your personal funds are not tied to business obligations. This separation is especially important for LLCs and corporations, which are designed to shield owners from personal liability.

Make Better Financial Decisions

Mixing personal and business funds can create confusion about your actual profits and expenses. You might overestimate revenue or overlook deductible expenses, leading to overpaid taxes.

When your finances are separated, you can clearly see how much money your business is generating and where it’s going. This visibility allows you to make smarter decisions, like when to reinvest profits, hire employees, or purchase new equipment. It also makes it easier to spot trends in cash flow, plan for slow periods, and forecast growth.

Build Credit History (and Access Financing)

It’s essential to establish your business’s credit history separately from your personal credit.

Lenders may consider your personal credit, but they also want to see that your business manages its obligations responsibly.

Opening accounts in your company’s name helps establish it as a separate entity with its own credit profile, which can make it easier to qualify for loans, credit cards, or vendor financing in the future.

Access Business-Specific Financial Features

Business accounts come with features designed for company needs, not personal use.

These can include invoicing tools, online payment processing, merchant services, and integration with accounting software like QuickBooks. Using accounts with these capabilities helps you manage your finances more professionally.

How To Keep Business and Personal Finances Straight

Convinced?

Perfect, then let’s get your business finances up and running.

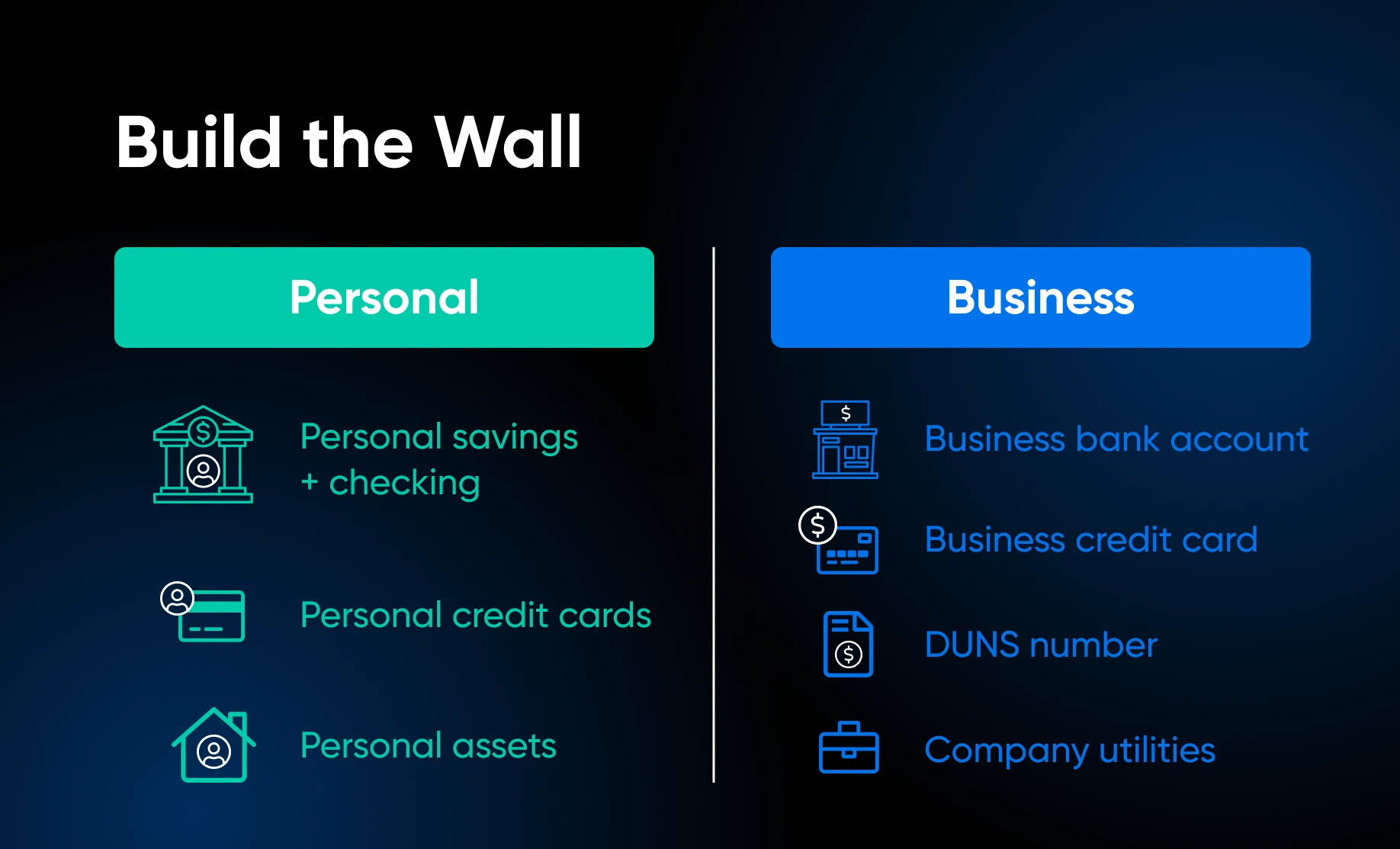

Open a Dedicated Business Bank Account

This is the ground floor. A business bank account is the foundation of financial separation.

All client payments should go into this account and all business expenses should come out of it. Keeping money separate makes tracking income and spending much simpler.

Use a Business Credit Card

A business credit card is another simple step with big benefits. It helps manage cash flow and tracks expenses automatically. Over time, it also builds your business credit.

Use it for business purchases only!

Get a DUNS Number

A DUNS number is a unique nine-digit identifier issued by Dun & Bradstreet.

This acts like a business credit score and links directly to your company’s credit profile. Vendors, creditors, and suppliers can use it to assess your business’s financial health and reliability.

A DUNS number can help you secure better loan terms, apply for business credit cards and grants, register as a vendor with private-sector partners and suppliers, track your credit report, and even expand into international markets.

A DUNS number is not an EIN or UEI – and knowing the difference matters.

EINs are tax identifiers issued by the IRS and are legally required for most businesses. UEIs (Unique Entity Identifiers) are federal identifiers required for any business contracting with the U.S. government – and as of 2022, the UEI replaced the DUNS number for federal procurement entirely.

If working with the federal government is part of your plan, you’ll register for a UEI through SAM.gov, not a DUNS. A DUNS number is voluntary and lives in the commercial world: vendor relationships, private loans, and credit applications outside the federal system.

Always Apply for Credit in Your Company’s Name

When seeking credit from suppliers or vendors, always use your company’s information on the application.

Trade credit allows suppliers and retailers to offer more favorable payment terms, typically ranging from net 310 to net 60 days.

This approach lets your business establish a credit history while buying products or services on credit and deferring payment for up to two months.

Set Up Company Utilities (if Applicable)

Any utility services used to primarily run your business should be set up in your company’s name.

Think phone lines, cell phone plans, internet, and cable services.

When your business handles these accounts, recurring operational costs get properly noted, which also helps build your company’s financial independence.

Insurance and Liability Protections To Consider

Even the best business structure and planning can’t cover every risk.

That’s why insurance is a critical layer of protection. Without it, a single claim could threaten your business and personal finances.

General Liability Insurance

General liability insurance is the baseline for most small businesses.

This covers accidents, injuries, or property damage caused by your business activities. If a client slips in your office or you accidentally damage a client’s property, this is the kind of insurance policy that protects you in these cases.

Professional Liability Insurance

Service-based businesses should consider professional liability insurance, also called errors and omissions insurance.

It covers issues that arise when clients claim you made a mistake in your advice or work.

For example, if a client were to threaten legal action over a missed deadline they believed impacted their business, professional liability insurance would step in to help.

Workers’ Compensation Insurance

This one’s kind of a no-brainer because if you have employees, workers’ compensation insurance is usually required.

This type of policy covers injuries or illnesses that happen on the job. It protects both your employees and your business from costly claims.

Business Property Insurance

Even if you work from home, business property insurance is worth considering.

It covers any expensive tools, equipment, or inventory you use if they’re damaged or stolen. Losing these items could halt your operations if you don’t have insurance that can help you replace them quickly.

Talk to an insurance agent to make sure you have the right coverage for your business size and industry.

Tax Planning Tips for Full-Time Entrepreneurs

Taxes are one of the biggest stressors for new business owners.

But with the right strategies, you can stay organized, reduce your tax bill, and avoid nasty surprises.

Track Income and Expenses in Real Time

For the love of all things holy, please use real bookkeeping software.

Popular options include QuickBooks, Xero, and Wave.

These types of tools make it easy to track income and expenses as they happen. This is helpful so that you don’t miss deductions and you get the clearest picture possible of revenue, costs, and profitability.

Set Aside Money for Taxes

This one’s gonna hurt.

Tax pros recommend setting aside about 30%-40% of your business income to safely cover federal and state taxes. Many entrepreneurs pay quarterly estimated taxes to avoid a big bill at year-end; sometimes this is required — check with a tax professional.

Keep this money in a separate savings account. This prevents accidental spending and ensures you’re always prepared.

Of course, tax obligations can vary a ton by business. For a more precise figure, or to find out if you can save less, consult a CPA.

Maximize Deductible Expenses

Deductible expenses reduce your taxable income. Common deductions include software subscriptions, office supplies, marketing, travel, and a portion of your home office if you work from home.

And if your business is an S corp, paying yourself a reasonable salary and taking extra profits as distributions can lower self-employment taxes.

A tax professional can help you find even more opportunities here.

Use Retirement Accounts

Contributing to a retirement account can lower taxable income now, all while helping you save for the future.

Plus, you should be setting aside money for this, anyway!

For more support when it comes to taxes, the IRS offers dedicated resources for small businesses and the self‑employed. It provides tax forms, guidance on filing and paying business taxes, information on deductions and credits, and resources to stay compliant with federal tax requirements.

Setting up your small business for longevity is all about how effectively you cover key financial and legal points.

Start laying a strong foundation by choosing the right structure (like an LLC or S-corp) to protect your personal assets and manage taxes effectively. Once that’s in place, separate your business and personal finances immediately by opening dedicated accounts to stay organized and simplify tax filing.

Next, build business credit through tools like vendor accounts and a DUNS number, and protect your operations with essential insurance such as general liability, professional liability, and property coverage.

Finally, establish strong tax habits early: Track income and expenses consistently, set aside 30–40% for taxes, and take advantage of deductions to reduce taxable income.

Together, these steps create a secure financial system that reduces risk, improves clarity, and supports long-term business growth!

[Download] 2026 From Side Hustle to Full-Time Business

Are You Ready for Takeoff?

Entrepreneurs spend 36% of every work week on admin tasks alone. This 46-page ebook gives small business owners a complete playbook for going full time — financial readiness, legal setup, online presence, time management, marketing, and hiring.

Get The Playbook

Did you enjoy this article?